Before you buy a home, it’s important to plan ahead. While most buyers consider how much they need to save for a down payment, many are surprised by the closing costs they have to pay. To ensure you aren’t caught off guard when it’s time to close on your home, you need to understand what closing costs are and how much you should budget for.

What Are Closing Costs?

People are sometimes surprised by closing costs because they don’t know what they are. According to Bankrate:

“Closing costs are the fees and expenses you must pay before becoming the legal owner of a house, condo or townhome . . . Closing costs vary depending on the purchase price of the home and how it’s being financed . . .”

In other words, your closing costs are a collection of fees and payments involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include:

Government recording costs

Appraisal fees

Credit report fees

Lender origination fees

Title services

Tax service fees

Survey fees

Attorney fees

Underwriting Fees

How Much Will You Need To Budget for Closing Costs?

Understanding what closing costs include is important, but knowing what you’ll need to budget to cover them is critical, too. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $366,900. Based on the 2-5% Freddie Macestimate, your closing fees could be between roughly $7,500 and $18,500.

Keep in mind, if you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

What’s the Best Way To Make Sure You’re Prepared at Closing Time?

Freddie Mac provides great advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

Work with a team of trusted real estate professionals to understand exactly how much you’ll need to budget for closing costs. An agent can help connect you with a lender, and together your expert team can answer any questions you might have.

Bottom Line

It’s important to plan for the fees and payments you’ll be responsible for at closing. Let’s connect so I can help you feel confident throughout the process.

Bottom Line

It’s important to plan for the fees and payments you’ll be responsible for at closing. Let’s connect so I can help you feel confident throughout the process.

67% of Americans say a housing market crash is imminent in the next three years. With all the talk in the media lately about shifts in the housing market, it makes sense why so many people feel this way. But there’s good news. Current data shows today’s market is nothing like it was before the housing crash in 2008.

Back Then, Mortgage Standards Were Less Strict

During the lead-up to the housing crisis, it was much easier to get a home loan than it is today. Banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance an existing one.

As a result, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices. Today, things are different, and purchasers face much higher standards from mortgage companies.

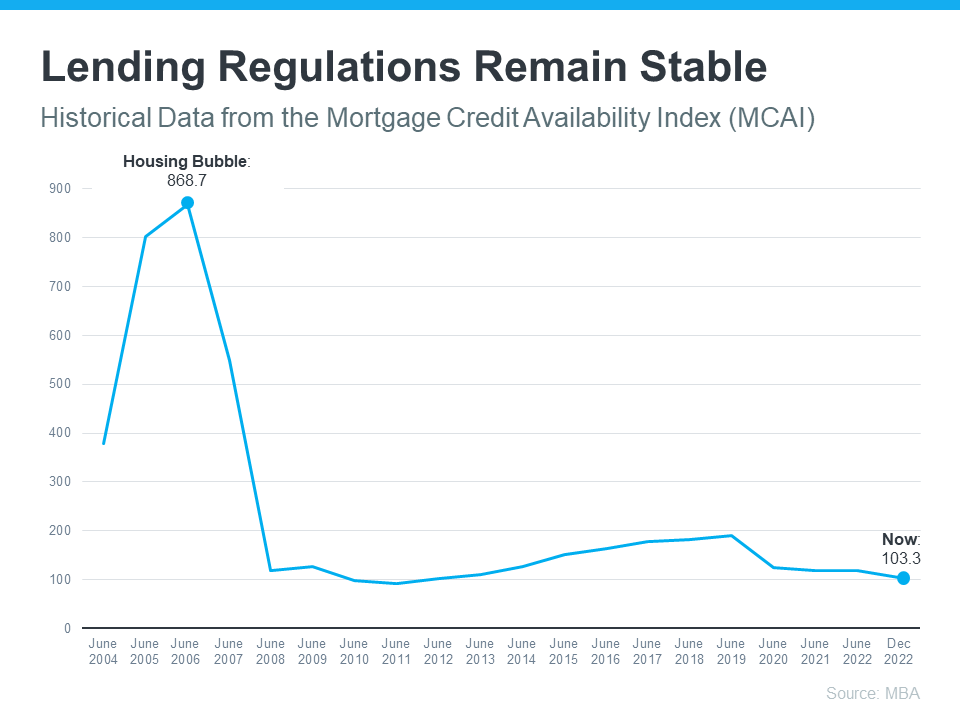

The graph below uses data from the Mortgage Bankers Association (MBA) to help tell this story. In this index, the higher the number, the easier it is to get a mortgage. The lower the number, the harder it is.

This graph also shows just how different things are today compared to the spike in credit availability leading up to the crash. Tighter lending standards have helped prevent a situation that could lead to a wave of foreclosures like the last time.

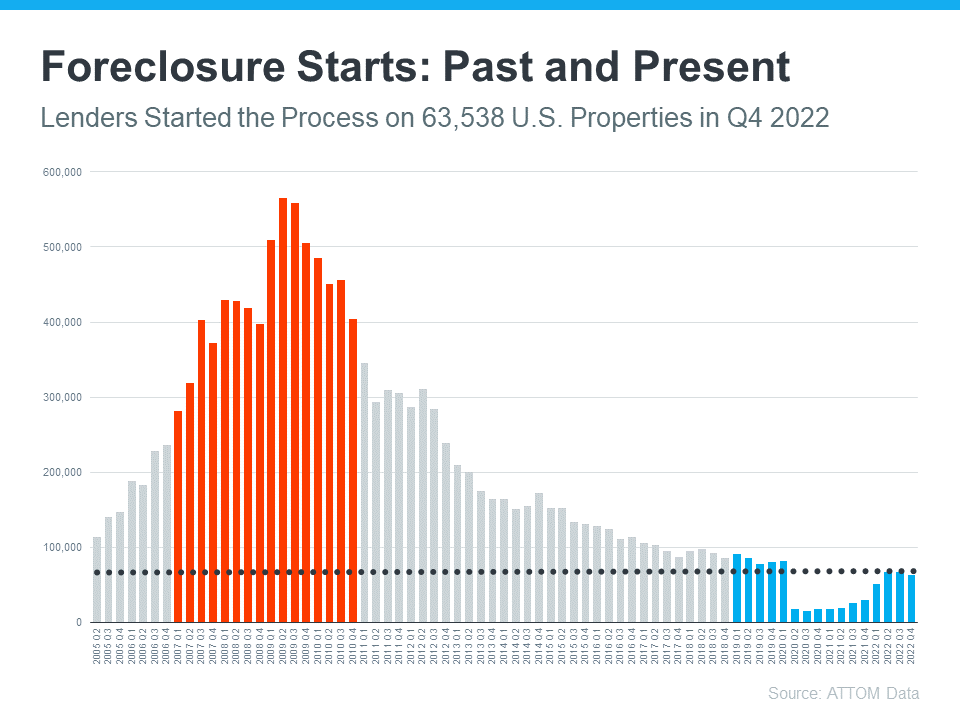

Foreclosure Volume Has Declined a Lot Since the Crash

Another difference is the number of homeowners that were facing foreclosure when the housing bubble burst. Foreclosure activity has been lower since the crash, largely because buyers today are more qualified and less likely to default on their loans. The graph below uses data from ATTOM to show the difference between last time and now:

So even as foreclosures tick up, the total number is still very low. And on top of that, most experts don’t expect foreclosures to go up drastically like they did following the crash in 2008. Bill McBride, Founder of Calculated Risk, explains the impact a large increase in foreclosures had on home prices back then – and how that’s unlikely this time.

“The bottom line is there will be an increase in foreclosures over the next year (from record level lows), but there will not be a huge wave of distressed sales as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.”

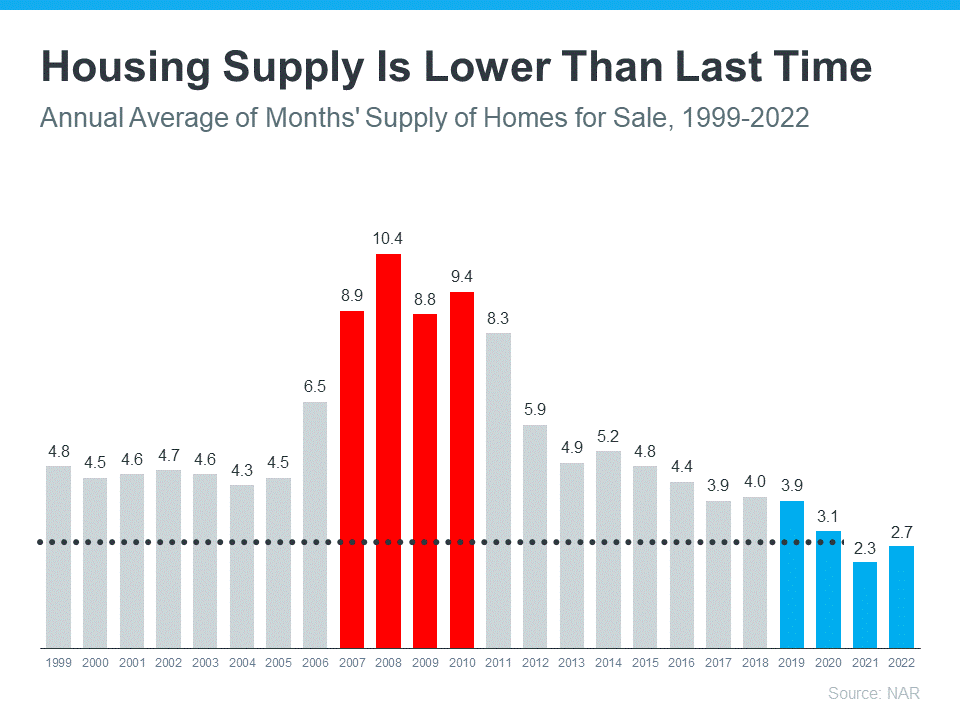

The Supply of Homes for Sale Today Is More Limited

For historical context, there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Supply has increased since the start of this year, but there’s still a shortage of inventory available overall, primarily due to years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just 2.7-months’ supply at the current sales pace, which is significantly lower than the last time. There just isn’t enough inventory on the market for home prices to come crashing down like they did last time, even though some overheated markets may experience slight declines.

Bottom Line

If recent headlines have you worried we’re headed for another housing crash, the data above should help ease those fears. Expert insights and the most current data clearly show that today’s market is nothing like it was last time.

If you’re a renter, you likely face an important decision every year: renew your current lease, start a new one, or buy a home. This year is no different. But before you dive too deeply into your options, it helps to understand the true costs of renting moving forward.

In the past year, both current renters and new renters have seen their rent go up based on information from realtor.com:

“Three out of four renters (74.2%) who have moved in the past 12 months reported seeing their rent increase. The strain from recent rent hikes isn’t exclusive to renters who have recently moved. Nearly two-thirds of renters (63.2%) who have lived in their current rental between 12 and 24 months, and likely renewed their lease, have also reported increases in their rent.”

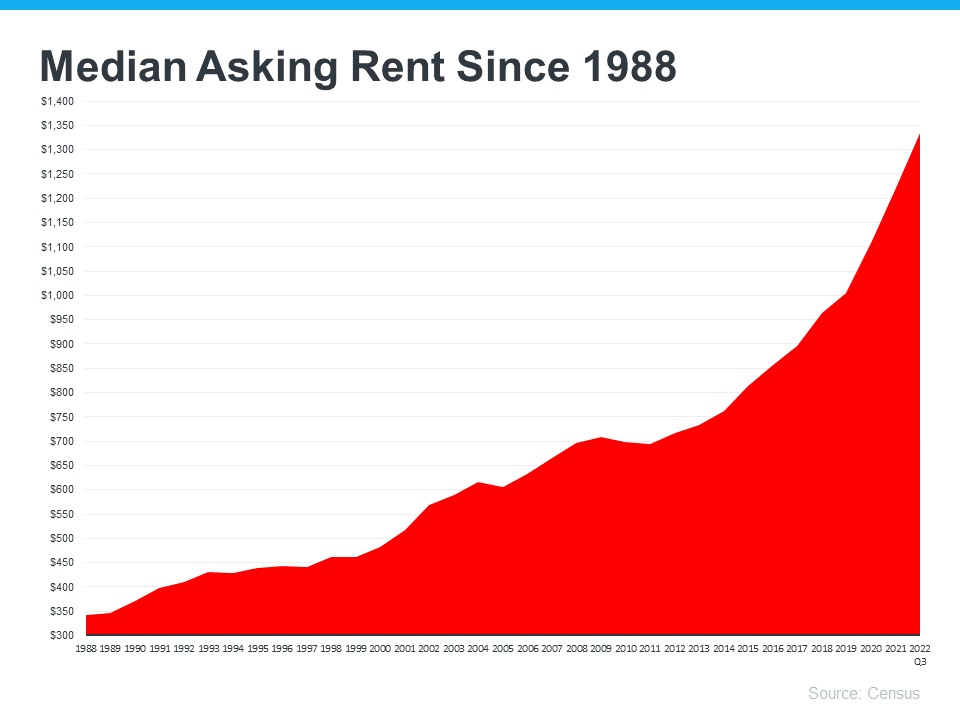

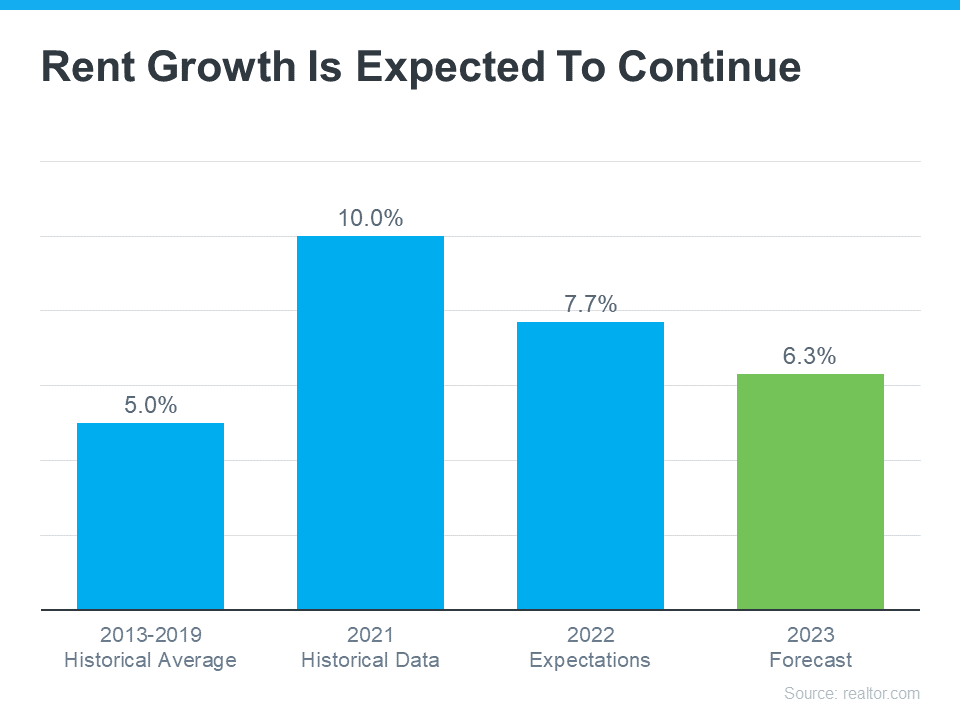

And if you look back at historical data, that shouldn’t come as surprise. That’s because, according to the Census, rents have been rising fairly consistently since 1988 (see graph below):

So, if you’re considering renting as an option in 2023, it’s worth weighing whether this trend is likely to continue. The 2023 Housing Forecast from realtor.com expects rents will keep climbing (see graph below):

That forecast projects rents will increase by 6.3% in the year ahead (shown in green). When compared to the blue bars in the graph, it’s clear that the 2023 projection doesn’t call for an increase as drastic as the ones renters have seen over the past two years, but it’s still above the historical average for rent hikes between 2013-2019.

That means, if you’re planning to rent again this year and you’ve not yet renewed your lease, you may pay more when you do.

Homeownership Provides an Alternative to Rising Rents

These rising costs may make you reconsider what other alternatives you have. If you’re looking for more stability, it could be time to prioritize homeownership. One of the many benefits of owning your own home is it provides a stable monthly cost that you can lock in for the duration of your loan. As Freddie Macsays:

“Monthly rent payments may increase over time, but a fixed-rate mortgage will ensure that you’re paying the same amount each month. With a fixed-rate mortgage, your interest rate is locked in for the life of loan. Steady payments allow you to budget wisely and make plans for the future.”

If you’re planning to make a move this year, locking in your monthly housing costs for the duration of your loan can be a major benefit. You’ll avoid wondering if you’ll need to adjust your budget to account for annual increases like you would if you left your housing payment up to your landlord and their renewal cycle.

Homeowners also enjoy the added benefit of home equity, which has grown substantially. In fact, the latest Homeowner Equity Insight report from CoreLogic shows the average homeowner gained $34,300 in equity over the last 12 months. As a renter, your rent payment only covers the cost of your dwelling. When you pay your mortgage on a house, you grow your wealth through the forced savings that is your home equity.

Bottom Line

If you’re thinking of renting this year, it’s important to keep in mind the true costs you’ll face. Let’s chat to see how you can begin your journey to homeownership today.

A new year brings with it the opportunity for new experiences. If that resonates with you because you’re considering making a move, you’re likely juggling a mix of excitement over your next home and a sense of attachment to your current one.

A great way to ease some of those emotions and ensure you’re feeling confident in your decision is to keep these three best practices in mind.

1. Price Your Home Right

The housing market shifted in 2022 as mortgage rates rose, buyer demand eased, and the number of homes for sale grew. As a seller, you’ll want to recognize things are different now and price your house appropriately based on where the market is today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Price your home realistically. This isn’t the housing market of April or May, so buyer traffic will be substantially slower, but appropriately priced homes are still selling quickly.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be.

2. Keep Your Emotions in Check

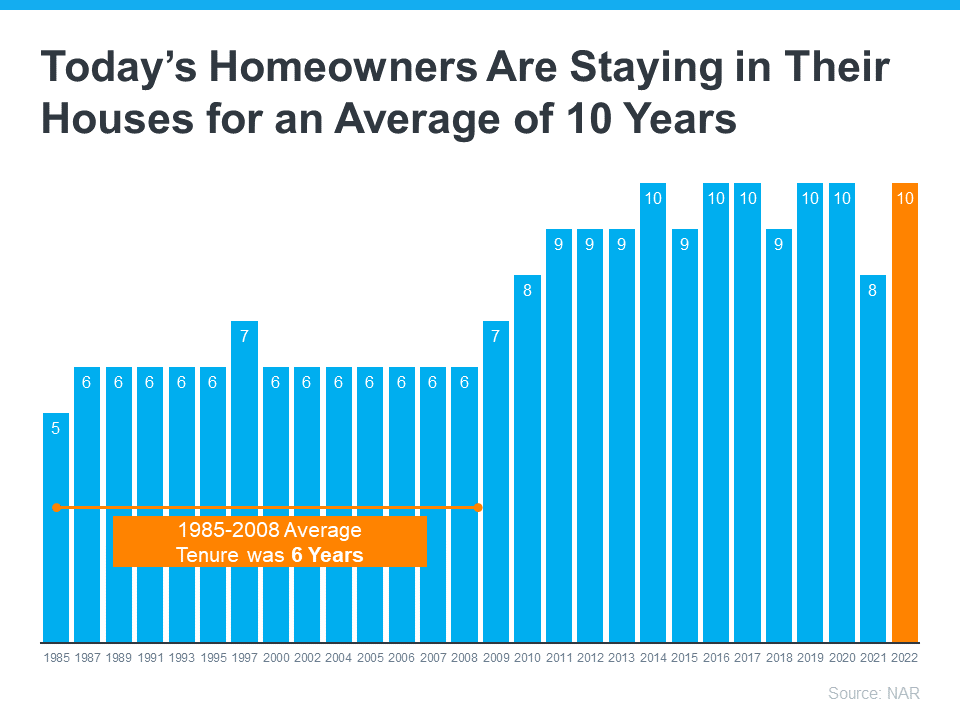

Today, homeowners are living in their houses longer. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 5 to 10 years (see graph below):

This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even harder to negotiate and separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

3. Stage Your Home Properly

While you may love your decor and how you’ve customized your home over the years, not all buyers will feel the same way about your design. That’s why it’s so important to make sure you focus on your home’s first impression so it appeals to as many buyers as possible. As NAR says:

“Staging is the art of preparing a home to appeal to the greatest number of potential buyers in your market. The right arrangements can move you into a higher price-point and help buyers fall in love the moment they walk through the door.”

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. A real estate professional can help you with tips to get your house ready to sell.

Bottom Line

If you’re considering selling your house, let’s connect so you have the help you need to navigate through the process while prioritizing these best practices.

Are you thinking about selling your home? It’s a big decision, and it’s natural to want all the help you can get. That’s why I’m sharing my best advice and I’ve compiled it into a few key tips. Whether your goal is to attract high offers, sell quickly, or just make the process go smoothly, these strategies will help you get the best possible results.

One of the most effective ways to sell your home fast and get the returns you want is to work with a professional real estate agent. Not only do they have the expertise to help you with tasks like pricing, marketing, and negotiations, but they also often have a network of connections to help you prepare your home for sale. It’s no surprise, then, that only 10% of homes are sold by owner (FSBO), according to the National Association of Realtors® (NAR). In fact, a NAR report found that the median FSBO home sells for $105,000 less than homes sold with the help of an agent.

As the housing market continues to adjust in 2023, it’s important to remember that buyers are no longer as eager to make offers above the listing price, waive contingencies, or get into bidding wars. Instead, top agents are advising motivated sellers to focus on tried-and-true strategies. Here are some tips to help you sell your home successfully:

Work With A High Quality Agent

Did you know that a top agent can help clients sell their homes for up to 10% more than the average real estate agent? When you work with me you’ll get the same hard work, attention to detail, and marketing that my team and I provide to everyone.

Enhance the interior of your home

If you want to show off your home’s value to potential buyers, start by making some improvements to the interior. These are some of the most impactful changes you can make:

Tackle repairs and upgrades: One of the quickest ways to set your home up for a fast sale is to tackle any deferred maintenance and necessary repairs. However, it’s important to do your research and focus on the upgrades that will give you the highest return on investment (ROI) and that are in high demand in your area. To get a sense of current preferences, you can visit open houses in the neighborhood, or you can hire a professional to conduct a pre-listing inspection. This will help you identify any essential repairs that could hold up the sale of your home later on. I also help my clients in their decision making by advising them about what people are looking for and touring their home before they start renovations or improvements.

Deep clean the interior: A thorough cleaning can help you sell your home in several ways. It prevents potential buyers from getting distracted by dirt or clutter, enhances the features of your home that might otherwise go unnoticed, and reassures buyers that there aren’t any other neglected amenities hiding in your home. For older homes in particular, it might be worth hiring a professional cleaning service to make sure every corner is sparkling.

Depersonalize and stage the space: It’s important to remove personal items and clutter from your home to make it easier for buyers to envision themselves living there. You should also consider staging the space to highlight the best features of your home and make it feel more inviting. This might involve rearranging furniture, adding some pops of color with decorative accessories, or bringing in some greenery to add life to the space.

Improve your home’s curb appeal

The first thing buyers see when they pull up to your home is the exterior, so it’s important to make a good impression. Here are some ways to enhance your home’s curb appeal:

Spruce up the landscaping: A well-manicured lawn and nicely trimmed bushes can go a long way in creating a positive first impression. If your landscaping is looking a bit overgrown, consider hiring a professional to tidy it up. You might also want to add some colorful flowers or potted plants to add a splash of color.

Touch up the paint: If your home’s exterior is looking a bit shabby, a fresh coat of paint can make a big difference. Choose a neutral color that will appeal to a wide range of buyers, and be sure to pay attention to details like trim and shutters.

Add some exterior lighting: Exterior lighting can create a warm and welcoming ambiance, and it’s also a practical feature that can help with safety and security. Consider adding some lanterns, sconces, or floodlights to highlight your home’s best features.

Be flexible and open to negotiation

While it’s important to have a clear idea of what you want to get out of the sale of your home, it’s also crucial to be open to negotiation. Buyers may come to the table with requests or counteroffers, and it’s up to you to decide whether or not you’re willing to compromise. It can be helpful to have a real estate agent by your side to advise you on what’s reasonable and what’s not.

Price your home correctly

Pricing your home correctly is essential to attracting buyers and getting the best possible return on your investment. If you price your home too high, it may sit on the market for too long and turn off potential buyers. On the other hand, if you price it too low, you’ll leave money on the table. A real estate agent can help you determine the right price based on market conditions and local demand, as well as the features and condition of your home.

By following these tips, you’ll be well on your way to a successful and profitable home sale. With the right strategy and a little bit of effort, you can achieve your home selling goals.

Contact me today to start a conversation about selling your home and how I can help you all throughout the process.